Is software's decades-long dominance of technology value creation coming to an end?

For twenty years, the consensus has been clear: software businesses with near-zero marginal costs, network effects, and scalable economics represent the pinnacle of corporate value creation. Yet recent market action suggests we may be witnessing a fundamental regime change—one where AI simultaneously commoditizes existing software while creating unprecedented demand for hardware, robotics, physical infrastructure, and the integration of digital intelligence with the material world.

At FGEN, we generally avoid commenting on short-term market fluctuations. However, developments over the past three months confirm observations we've been making for over a year.

The SaaS sector faces existential margin compression as AI models replicate functionality at dramatically lower costs. Meanwhile, value migrates toward companies at the intersection of software and hardware: those building physical infrastructure for AI compute, manufacturing robots and autonomous systems, and controlling materials and energy resources.

The S&P 500’s double-digit 2025 returns masked massive sectoral shifts. The commodity sector, in particular, needs closer examination.

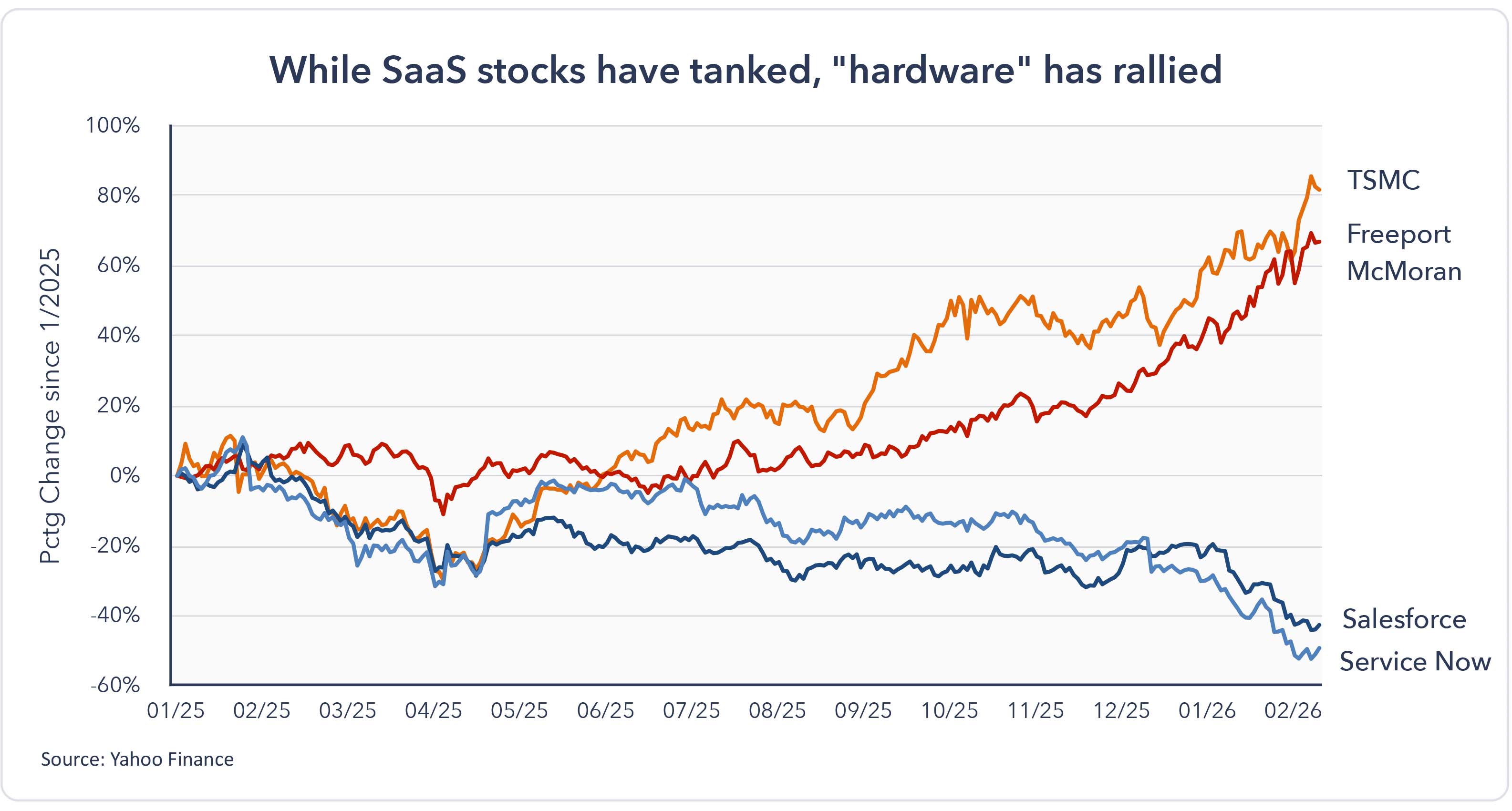

Beyond the well-documented gold and precious metals rally, base metals surged, with major commodity producers such as Rio Tinto, Freeport McMoran and BHP rallying sharply. The uranium market also saw a steep rise, a development largely overlooked by mainstream commentary.

These moves are a manifestation of the AI narrative: the "resource grab" story, with physical constraints on compute infrastructure, increasingly apparent. The buildout of data centers, the manufacturing of advanced semiconductors, and energy requirements are creating unprecedented demand for physical resources.

The second, more dramatic development is the accelerating disruption within the Software-as-a-Service (SaaS) sector. Major players like Salesforce, ServiceNow, and Adobe have been trending down for a year. Then mid-tier SaaS stocks also took steep dives in recent weeks. The catalyst came with Anthropic's release of a legal assistant add-on for Claude, which crystallized investor fears about AI displacement—a process that, like the bankruptcy in Hemingway’s novel, happened "gradually, then suddenly."

It took a wave of disappointing earnings reports, some improvements in AI models, and the release of a seemingly innocuous add-on from AI startup Anthropic to suddenly wake up investors en masse to the threat. The result has been the biggest stock selloff driven by the fear of AI displacement that markets have seen. Shares of software companies including Microsoft, Salesforce, Oracle, Intuit, and AppLovin tumbled, dragging down the technology sector and weighing on the broader stock market.

For months, analysts debated whether AI would complement or displace existing software businesses. The market's answer, delivered with sudden clarity, suggests displacement appears more probable than many assumed.

Software companies that spent decades building moats around proprietary data, user interfaces, and workflow integrations are discovering that AI models can replicate much of this functionality with remarkable speed. The nature and velocity of the decline reflecting fundamental business model concerns rather than cyclical rotation.

Fifteen years ago, Marc Andreessen observed that "software is eating the world." His insight captured the digitization of industry after industry—retail, media, communications, finance—as software-based businesses displaced physical incumbents. Business models with near-zero marginal costs and network effects generated unprecedented valuations.

Today, we are witnessing a reversal. The bottleneck in AI value creation is shifting from code and algorithms to physical constraints—semiconductor manufacturing capacity, energy availability, cooling infrastructure, and raw materials.

This manifests in multiple ways. Datacenter construction has become a limiting factor for AI capability deployment. TSMC's advanced chip fabrication capacity is perhaps the most critical bottleneck in the entire AI value chain. Power grid capacity in regions hosting major data centers is being stressed to unprecedented levels. These are physical, capital-intensive challenges that cannot be solved with clever code.

The physical bottlenecks constraining AI deployment, however, create opportunities in sectors where hardware has always mattered. The defense sector exemplifies this. Autonomous drone systems now make use of AI models for real-time decision-making and coordination. Simultaneously, they need substantial physical resources: steel for airframes, copper for motors, rare earth elements for electromagnets and sensors, and advanced materials for stealth capabilities. The next generation of military technology is neither purely digital nor purely mechanical – it needs both computational sophistication and material abundance.

Similar patterns are emerging across other sectors. Autonomous vehicles require AI for navigation and decision-making, plus hardware including sensors, computing platforms, and electric drivetrains with significant material requirements. Smart manufacturing combines AI-driven optimization with robotics and physical automation. Healthcare applications of AI increasingly depend on specialized hardware for imaging, diagnostics, and robotic surgery.

We believe this represents a fundamental shift in how AI creates value. The previous software era operated in the realm of electrons. AI's trajectory, however, demands integration with atoms: robots that manipulate physical objects, autonomous systems that navigate real-world environments, manufacturing equipment that transforms raw materials, energy infrastructure that powers compute, and sensors that bridge the digital and physical worlds.

Success requires capabilities across both domains, favouring integrated players or those with strong partnership ecosystems. The pure software business model, while not obsolete, occupies a narrower strategic position than it did a decade ago.

We are experiencing a fundamental reordering of technology value creation that will define the next decade. Software dominance is giving way to hardware primacy where physical constraints determine who captures AI's economic value.

We believe this transition will be volatile. Sectors and companies that appeared structurally advantaged face margin compression and displacement. Meanwhile, those bridging the digital and physical worlds are reasserting strategic importance.

As AI capabilities advance, the physical infrastructure and the hardware systems will become more critical. The resource grab in commodity markets reflects rational positioning for this reality, but the story extends to the entire value chain of physical AI deployment.

Those that recognize this shift earliest will likely emerge as the next decade's winners. Those anchored to software-era assumptions risk being left behind as technology value creation fundamentally transforms.

AI is commoditizing software while driving new demand for physical infrastructure, marking a shift from bits to atoms that could define the decade ahead.

AI investments look excessive until you know what you're really looking at: knowledge engines that compound indefinitely, fuel decades of growth and drive tomorrow's innovation.

Explores how USD depreciation enhances GCC resilience via Asian export booms, diversification, and tourism inflows, positioning the region as a stable haven for global investors.